This post takes a long overdue look at the monetary, financial, economic and political developments that took place during 2012 and the trends at the end of the year. It’s an exercise in taking stock and follows a relatively simple format orientated by the rudimentary, but not irrelevant, IS-LM/AD-AS approach before concluding with some remarks about the evolution of European party political systems.

During 2012 the monetary base continued to increase, thanks to accommodating central banks’ expansion of their balance sheet in the Euro-Zone and the UK. Meanwhile intervention in the USA and Japan continued, but was balance sheet neutral. Monetary policy has kept interest rates at historically low levels and financed government debt, which has led to historically low bond yields. These in turn have created what is likely to be a bond market bubble, which can be seen in some historically low pricing of corporate bonds.

Meanwhile, the expansion of the monetary base is not paralleled in the broader monetary supply. This is appears to be motivated by low growth expectations, caused by a difficult economic environment, in the EMU and in the UK. However, the situation is better inthe USA and Japan, where the expansion in their respective central banks’ balance sheets appears to have covered the gap dug by the financial crisis. Certainly, the MBS targetted QE of the Fed has helped the USA economy, as has the lack of austerity and the status of the $US as the world’s reserve currency. In the Euro-zone, the same is not true so that much of the uncertainty about the future growth of the currency area appear to be tied to expectations about its institutional fate.

The consequence is a stagnant real economy, particularly so in the UK and in Europe, while deflation in Japan continues although with hopes of reflation. Finally, the chaos of elections, austerity and uncertainty that has been plaguing the Euro-Zone is clearly disrupting the old party-political systems and causing previously marginal parties to gain an increasing share of voters’ intentions. The frustration of voters tied in their rusting golden straight jacket is most vivid in Greece where PASOK has been obliterated and where Syriza appears the new voice of the left, while Golden Dawn glooms darkly over a desperate and impoverished society, where grasping at straws and holding to their pride people begin to turn on each-other.

Unfortunately, this post fails to consider China, Brazil and the rest of Latin America, Southeast Asia, Africa and the Middle East, which given recent recent developments appear to be the most interesting. In time, hopefully, I will have the opportunity to look at them too.

LM: Money Supply – Interest Rates and Currency Wars

Beginning with the basic contributor to the price of money, 2012 saw few changes in official interest rates. Among the world’s biggest banks, only the ECB lowered its interest rate on July 5th. Otherwise, Australia, Israel, Sweden, Hungary, Poland, Korea, Brazil, the Czech Republic, South Africa, Denmark, China, India, Norway, Indonesia and Chile lowered their interest rates.

There are two reasons for this. First, developed economies continued to falter under the weight of the Euro-Zone sovereign debt crisis and Japanese deflation, there’s an incentive for their central banks to allow cash to remain artificially cheap in the hope that it will stimulate the economy back into shape. The reason the Fed, the BoE and the BoJ did not lower rates further during 2012 is that they are pretty much at zero, as it is. The ECB decreased in the rate on July 5th, but this was not very successful and the priority of its Governing Council is now to fix the channel of monetary policy transmission. Secondly, the devaluative initiative taken by developped economies at the onset of the crisis continues to pressure other economies to devalue their currencies to maintain the competitiveness of their exports. Basically, recession leads to low interest rates, which devalues the currency and leads to a realignment in the balance of payments (BoP). Because realignments in large economies spillover to their neighbours, this leads to a currency war-like dynamic. Everyone lowers its interest but relatively speaking, no one’s currency really depreciates. Asides in gold terms…

LM: Money Supply – Cash Injected by Central Banks

So we know that the world’s largest central banks have maintained a low level of short term interest rates, and that the rest of the world started catching on. But what have the world’s largest central banks been doing with their balance sheets?

While the balance sheet of the FED has changed relatively little in the last year, according to the Cleveland Federal reserve,  …the same cannot be said of the BoE, whose balance sheet increased by a whopping GBP125bn.

…the same cannot be said of the BoE, whose balance sheet increased by a whopping GBP125bn. Most importantly to this website, the LTROs in the first quarter of 2012 continued fueling the increase in the size of the ECB’s assets.

Most importantly to this website, the LTROs in the first quarter of 2012 continued fueling the increase in the size of the ECB’s assets. Finally, the BoJ’s balance sheet grew approximately by JPY20tn, to only a couple of a trillion shy of JPY160tn. The push was overwhelmingly driven by purchases in government debt.

Finally, the BoJ’s balance sheet grew approximately by JPY20tn, to only a couple of a trillion shy of JPY160tn. The push was overwhelmingly driven by purchases in government debt.

Looking at these developments in terms of % of GDP can be useful to see the systemic importance of the world’s four largest central banks. The image below (found at alsosprachanalyst) shows that 2012 was the year when CB Balance Sheet/GDP ratios in the Euro-Zone and the UK exceeded those in Japan and the USA, respectively.

So the decrease in short term interest rates was accompanied by an explosion of bank balance sheets in the Euro-Zone, the UK and to a lesser extent in Japan.

LM: Monetary Base and Money Supply

It is interesting to notice that despite all of this buoyancy, the money growth stayed relatively stable in the last 12 months. Indeed, according to the following graph from Nomura, kindly provided by the FTAlphaville, the result of all the stimulus in the UK and in the Euro-zone has been rather limited. For a triplication in the monetary base (narrow money like currency and bank deposits with the CBs, which will grow due to the CBs’ balance sheet expansion) no similar rise took place in broad money.

The conclusion is that the CBs of the world continue to hold the world’s financial sectors in their hands, propping them until they can react again. CB money is still the only reason why the financial sector has not gone under. The money injected by the central banks has just filled the hole created by the asset destruction that followed the Financial Crisis-cum-Lehman Bankruptcy-cum-Euro-zone Sovereign Debt Crisis. Private money is going nowhere. As is clearly illustrated by the previously discussed dynamics of the current account-deposit account shifts in the Euro-Zone and the intra-Eurosystem imbalances, cash is staying in the financial market. It is shoring up bank balance sheets, going into government bonds and other perceived safe assets while the banks deleverage and desintermediate, forcing the central banks to intermediate and leverage themselves. The financial sector is therefore completely unrepresentative of the real economy, because it does not transmit its riches to it, much as has been advocated by the ECB’s Mario Draghi as a reason not to lower MRO rates further. Effectively, monetary policy has just been maintaining the status quo, flowing around the financial market but not entering the real economy.

To put it in economically (basic but) friendly terms, if you take the monetary exchange equation,

M has increased, to compensate for the fact that V has decreased. Most likely, because the decrease in V (number of time money is spent) was higher than the necessary increase in M (monetary base), Q (the amount of assets available for purchase) also fell, because of all the bankruptcies. As a result, P (price level) does not really rise. On the contrary, it may even fall.

LM: Money Demand – Sovereigns

Money makes its way into the real economy from the financial sector either via the private or the public sector. Here we look at the public sector.

So where did all the money go to? – In the USA, the FED has been intervening in the markets beyond its previously normal OMOs via Operation Twist (since September 21st 2011) and via QE. The first corresponds to the purchase of Long-term US Treasury notes financed by the sale of Short-Term note, in order to flatten the US Treasury yield curve. Because it is the system’s benchmark, this would hopefully bring down everyone else’s yield curve.

The second corresponds to the purchase of Mortgage-Backed Securities (MBSs) and is consider more in-depth in the next section.

The second corresponds to the purchase of Mortgage-Backed Securities (MBSs) and is consider more in-depth in the next section.

In the UK, the Lady of Threadneedle Street is growing fat on a steady ‘Gilty’ diet. According to the Bank of England, this is being done through the Bank of England Asset Purchase Facility Fund (BEAPPF), a subsidiary that was established

“with the initial objective of improving the liquidity of the corporate credit market by making purchases of high-quality private sector assets (…), the Fund is financed by loans from the Bank and those loans are included in “other assets” . They account for the bulk of the increase in “other assets” since March 2009. The Bank’s loans to the Fund were in the initial phase financed with a deposit by the government’s Debt Management Office with the Bank. Since March 2009, as already noted, the Bank’s loans have been financed by increased reserves liabilities on the Bank’s balance sheet. (…) The greatest part of the Fund’s purchases has been of gilts.”

Indeed, if you look at the holdings of Gilts (orange), the BoE now owns around 20%, up from none before the crisis.

Meanwhile, in Europe, and as mentioned in a previous post, because banks refuse to lend to each other the ECB has to intervene in order to intermediate the market, thus leading to the famous intra-Eurosystem Target2 imbalances (which seem to continue on their rebalancing path).  Comparing the data series, we also notice that a vast amount of that money (a little shy of €1tn) is sitting pretty at the ECB, initially in the deposit facility, earning some interest…

Comparing the data series, we also notice that a vast amount of that money (a little shy of €1tn) is sitting pretty at the ECB, initially in the deposit facility, earning some interest…

… to Core banks…  …before moving into the current accounts, after the July cut of the deposit facility to 0%.

…before moving into the current accounts, after the July cut of the deposit facility to 0%.

The rest, I am told, was handed out by the Italian and Spanish CBs to national banks…  …who used the funds to buy their respective government’s bonds.

…who used the funds to buy their respective government’s bonds.

All in all, all three major CBs have been on a government bond buying spree, so that the satndardised distribution of investors in US, UK, Euro-Zone and Japanese government bonds looks like this:

Meanwhile, in Japan the situation is fairly stable. Surprisingly, the BoJ is not as relevant for the Japanese government securities market as the later is for the first. According to a June quarterly estimate, Japanese banks and similar financial institutions represented 43% of the total JPY708.9tn of Japanese government bonds outstanding at end of 2012. Of the rest, the Bank of Japan only represented 10.2%, superseeded in its holdings by Insurance funds’ 19.1% and private and public pension funds’ aggregate holdings worth 1-34% of the total. The only category of investors worth more than 5% that held less than the BoJ was “Foreigners” who held a meagre 8.7%. Because domestic investors, particularly banks are less mobile in their investments than foreigners , this fact also explains relatively well why shorting Japanese government bonds continues to fail as an investment strategy.

In conclusion, it is clear that a lot of the money has gone to sovereigns. The increase of central banks’ balance sheets has been done through the purchase of government bonds or increase loans to banks who then go on to lend to governments, the present policies have facilitated a slower pace of deceleration in the growth of public sector debt. Granted that government deficits have been decreasing all over the world, after exploding as a response to the financial crisis, but slower than would have been the case had central banks not intervened.

Notice that this effort to deleverage has been more pronounced where the central bank is more independent, such as in the Euro-Zone, than where it is less so, such as in Japan, the UK or the USA. This is not only because of the ECB’s independence but also because of the lack of power of the Euro-Zone countries that require most deleveraging.

While it was a paradigm shifting event overall, the OMT announcement was particularly targetted at the funding of public sector entitites, including sovereigns. Indeed given that the year started on a pretty miserable note with S&P downgrading left and write across the Euro-Zone,

… the negative outlook proceeded with Spain, Italy, Portugal and Greece taking a beating throughout the year.

Even the Bank of England, in its November 2012 Inflation Report, noticed the very strong effect on the markets, first with the London announcement in July and then the actual announcement in September.

Meanwhile, less attention was paid to Greek, Irish and Portuguese bond yields, which have fallen substantially since the onset of 2012. In Greece, this was a turbulent transition that required a private sector bail-in (in February/March) and a second debt buyback (in December). In Ireland, it was done thanks to market confidence and good debt management that allowed the sovereign to conduct a successful bond switch and outright sale as well as issue new “amortising bonds” and repurchase and cancel EUR500m worth of debt in December. In Portugal, success was more tentative, but also saw the exchange of EUR3.757bn 2013 bonds for the same 2015 volume. Once again, the July/September OMT announcement(s) proved decisive.

Beyond these falling yields in the periphery, core Euro-Zone issuers, the US Treasury and the Japanese government offer even more oppressively low returns. Between January 6th and December 28th, 10yr government bond yields have fallen from 1.85% to 1.31% in Germany, from 1.95% to 1.38% in the USA and from 0.98% to 0.8% in Japan.

LM: Where is the Money Going to? – Corporates

Notwithstanding the falling returns of sovereign bond markets, fixed income continues to appeal to a growing number of investors. Data from the European Fund and Asset Management Association (EFAMA) confirms trends that the media has been covering during the year. With contractionary economic dynamics across the world, equity funds have seen a drop in activity. The same outflow has been experienced by money market funds, due to historically low interest rates across the world.  A somewhat clearer but less granular picture is given through EPFR data in this BoE chart.

A somewhat clearer but less granular picture is given through EPFR data in this BoE chart.

This flow into fixed income is driven by banking desintermediation in the wake of Basel III, which is driving corporates of all ratings to issue bonds

This has allowed prime rated issuers such as Phillip Morris’ 12yr bond at 2.9% in May, Nestle’s EUR500m 4yr bond at 0.75% in October or TeliaSonera’s 15yr at 3% in November to issue the cheapest ever corporate bonds. At the other extreme of the credit rating spectrum, an increasing number of junk rated corporates continued to borrow in bond markets at very low rates (which move in the opposite direction of the price of the ETF below).

This has allowed prime rated issuers such as Phillip Morris’ 12yr bond at 2.9% in May, Nestle’s EUR500m 4yr bond at 0.75% in October or TeliaSonera’s 15yr at 3% in November to issue the cheapest ever corporate bonds. At the other extreme of the credit rating spectrum, an increasing number of junk rated corporates continued to borrow in bond markets at very low rates (which move in the opposite direction of the price of the ETF below).

This transmission to the real economy is enhanced in the USA by QE programmes through which the Fed purchases Mortgage-Backed Securities (MBSs) . This is motivated by a belief that real-estate is a fundamental channel of funding for SMEs, which are the backbone of the economy and fundamental for job creation, assuming that entrepreneurs will mortgage their homes in order to fund their economic enterprises. By going into the MBS market, the Fed is hoping to revive the stagnant US economy and drop the high (by US historical standards) level of unemployment. Recent experiences however suggest that the latter might be ill-founded and may instead lead to another credit-fuelled consumption bubble, while the first may facilitate the postponement of inevitable reforms in the USA, the eventual reckoning of which may end up being more chaotic than otherwise. The purchases, which exploded during the peak of the sub-prime crisis, have only recently returned. As a result of delays in MBS supply due to the volume of business limitations imposed on mortgage brokers, this has taken some time to pick up, but as we can see there’s been an recent upwards move in MBS holdings from the Fed.

QE continues in its third interation “QE3” announced in September, before the FOMC December announcement that “Operation Twist” was to be replaced by QE4, a purchasing programme that sees the Fed purchase long term US treasuries without sterilising it by selling at the short term.

LM: Where is the Money Going to? – HHs and Transmission of Market Conditions to the Real Economy

The implications of the desintermediation that is driving the fixed income boom mentioned above are rather negative for consumers, households (HHs) and SMEs. A more granular understanding of the isolation between the financial sector and the real economy can be provided by bank lending surveys, which show a contractionary environment in Europe and in the UK, but not so much in the USA and in Japan.

In the USA, the Fed’s October 2012 bank lending survey suggested an improvement in credit conditions. It

“reported easing standards for business lending”…

…”and some categories of consumer lending over the past three months”.

“Respondents reported little change in residential real estate lending standards on balance.”

“Significant fractions of banks reported a strengthening of demand for commercial real estate loans, residential mortgages, and auto loans, on balance, while demand for most other types of loans was about unchanged.”

According to the Bank of Japan January 2013 Survey of Bank lending conditions, conditions are also positive although improving at a slow rate. Demand for loans is on the rise be it from HHs, firms or local governments.

Demand has been supported by easing credit standards for firms and HHs, making it easier for those who can afford the rates to get the loans.

This rosy Japanese picture is only spoiled by the marginally rising costs of bank credit.

According to the third quarter 2012 bank lending survey which the ECB published in October, Euro-Zone consumers’ demand for consumer credit remained low but stable while it fell a bit for mortgage credit.

The dominating factor affecting these elevated credit standards was the negative economic expectations for economic growth, which is normal given the stagnating conjuncture.

This pessimism overlaps with the actual demand in the market, as consumer sentiment is probably driving consumers to spend less on durable goods that tend to have higher fixed costs. This is true of both consumer credit…

… and of mortgage demand.

At the same time, businesses (what the ECB calls “enterprises”) demanded less loans and credit lines.

Demand fell mostly on account of the smaller relevance of fixed income and mergers and acquisition, while debt restructuring seemed to facilitate some increase in credit demand.

Meanwhile, SMEs, which everybody agrees are the bread and butter of any economy’s labour market, have continued to struggle accessing finance. According to the ECB’s September survey of funding availability to SMEs.

Meanwhile, SMEs, which everybody agrees are the bread and butter of any economy’s labour market, have continued to struggle accessing finance. According to the ECB’s September survey of funding availability to SMEs.

“In the period from April to September 2012 (H2 2012), which was characterised by weakening economic activity in the euro area, a net 10% of euro area SMEs reported a contraction inturnover.”

This was driven by rising costs (labour and otherwise) and falling profits.

Meanwhile the funding structure remained unchanged, with overdrafts and credit lines dominating, followed by bank loans, leasing, hire purchase and factoring, while trade credit continued to come last. Although a little less than half of SMEs surveyed maintained that the availability had remained unchanged, the amount considering it had decreased appears to have increased more than those considering it has increased.

SMEs, perceived a deterioration of credit availability, across sources.

The main reason driving banks’ unwillingness to lend is due to the general economic outlook and a variable tautologically called “Willingness of bank to provide a loan“.

The main reason driving banks’ unwillingness to lend is due to the general economic outlook and a variable tautologically called “Willingness of bank to provide a loan“.

Ultimately, the main difficulty facing Euro-Zone firms is the macroeconomic conjuncture which makes them struggle to find new customers.

I won’t go into the same level of detail for the UK, but suffice it to say that although expectations were hopeful, the credit reality was similarly negative.

In conclusion, although there was an improvement of the American credit environment, this has not yet spilled over into Europe.

The Evolving Effect of the EZ Sovereign Debt Crisis

If we juxtapose the survey below with peripheral yields and forex movements we can see that perceptions of the impact of the Euro-Zone sovereign debt crisis evolve with the turbulence it creates, rather than foresee it.

The effect was low when the crisis was temporarily tamed by the LTROs, then it exploded during Q2 due to the political turmoil and uncertainty surrounding the Greek elections only to calm down during Q3, as markets expected what turned out to be the OMT announcement following the July comments from Draghi in London.

It is interesting that the VIX (for the USA) and VSTOXX (for Europe), so-called fear measures, have been tracking each other for most of their history. These co-movements are representative of the interdependence between the two economic blocs. Moreover, on very few occasions has Europe been less volatile than the USA. However, at the end of 2012, for the first time since the last quarter of 2008, Europe appeared less risky than the USA, on account of the unresolved fiscal cliff negotiations and the upcoming debt ceiling negotiations that are due to culminate at the end of February. Moreover, despite the resolution of the Fiscal Cliff in the first week of 2013, we are likely to see a rise in US fear at the end of February when yet another Debt Ceiling crisis is due to take place.

The peaks and troughs of 2012 described in the figure immediately above are mostly the result of developments in the Euro-Zone sovereign debt crisis, which were best tracked by EUR-USD fluctuations during the year. As was mentioned in the beginning of the post, the massive injections of cash did not do much in terms of devaluing any of the currencies by the end of the year.

Note that the figure above ignores a number of other events (For more details about elections and Euro-Zone measures, please click here, or read further).

IS – Fiscal Policy, Consumption, Investment and the balance of trade

In light of the aforementioned conditions in liquidity markets, and the turbulence created by the Euro-Zone sovereign debt crisis, it is not surprising to find a downbeat reality in the real economy with negative growth in most large economies in 2012, aside perhaps Japan and the USA (although the data below is provisional), consistent with bank lending conditions.

Consumption remains the largest contributor to GDP, particularly in the USA and the UK, although a slight increase that had taken place during the credit fueled years is slowly decreasing in relevance. Consumption continues to contribute 75% and 95% of nominal GDP.

This is confirmed at yearly as well as the more granular quarterly data level (for UK and Euro-Zone 17 only).

Meanwhile, Investment (as proxied by the Eurostat’s Gross Capital Formation) has taken a hit as a result of the decrease in value of several assets in inventory either through repricing or depreciation. Nonetheless, they continue to contribute between 15% and 20% of GDP.

Meanwhile, Investment (as proxied by the Eurostat’s Gross Capital Formation) has taken a hit as a result of the decrease in value of several assets in inventory either through repricing or depreciation. Nonetheless, they continue to contribute between 15% and 20% of GDP.

These proportions are also confirmed on a quarterly basis, with seasonal trends.

These proportions are also confirmed on a quarterly basis, with seasonal trends.

Moreover, the Euro-Zone remains the only economy that is able to run a surplus in its trade of goods balance, while the UK’s services export appear to be booming. Japan’s recent fall from export grace is probably one of the stronger motivations for the monetary easing that proves so popular with its people, thanks to its promise of a weaker currency and a return to a trade surplus.

Moreover, the Euro-Zone remains the only economy that is able to run a surplus in its trade of goods balance, while the UK’s services export appear to be booming. Japan’s recent fall from export grace is probably one of the stronger motivations for the monetary easing that proves so popular with its people, thanks to its promise of a weaker currency and a return to a trade surplus.

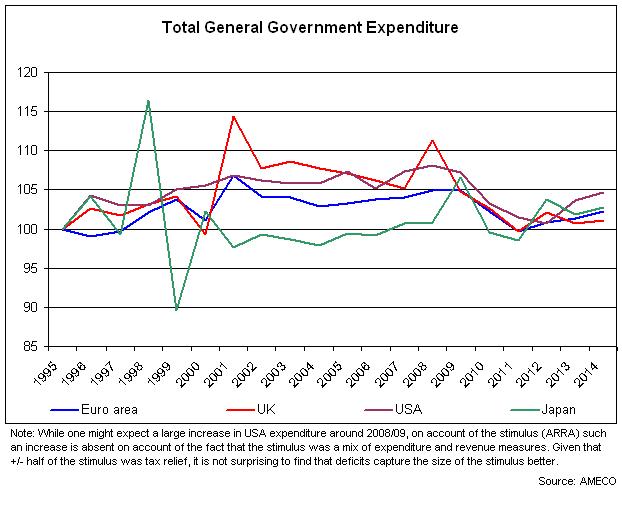

Finally, and despite initial fluctuations to cope with the beginning of the crisis, the fiscal austerity that the markets continue to impose on governments seems to constraint their ability to extend expenditure. Indeed, according to EU data, it would appear that it has barely grown in nominal terms since 1995. Once you adjust for inflation, the government’s real expenditure has decreased substantially.

Finally, and despite initial fluctuations to cope with the beginning of the crisis, the fiscal austerity that the markets continue to impose on governments seems to constraint their ability to extend expenditure. Indeed, according to EU data, it would appear that it has barely grown in nominal terms since 1995. Once you adjust for inflation, the government’s real expenditure has decreased substantially.

Inevitably, inflation has collapsed as this seems to be a contraction of economic activity motivated by demand dynamics fuelled by a destruction of money demand. Although oil shocks, money printing and government deficits have not allowed inflation to completely collapse, it has certainly decreased. Curiously, any nominal contractions discussed above are exaggerated in real terms for the Euro-Zone, the UK and the USA. However, in Japan, deflation pervades, rather than inflation, somewhat mitigating the real effects of the aforementioned contraction in economic activity.

BoP – Current and Financial Account Developments

The current account balances, include more than the trade of goods and services discussed above, showing that other transactions are mitigating US and Japanese current account deficits, but not necessarily the UK’s although a recent resurgence has taken place.

Finally, the financial account seems symmetric to the current account. In light of anecdotal evidence, it is not surprising to find the UK and the USA, two well known financial centres attracting financial surpluses, as money floods to their economies. Interestingly, both in its current and capital accounts, the imbalances are less pronounced for the USA’s economy, which is larger and more diversified in general, than the smaller open economy of the UK. Meanwhile, exporters such as the Euro-Zone and Japan, create surpluses which are then channeled abroad.

Clearly aggregated data misrepresents reality. According to the conditions described above, the Euro-Zone comes off as an extremely balanced economy. Of course the devil is in the detail. In the Euro-Zone, the trading desiquilibria are quite large. However, they did seem to be improving at the end of the year, a reaction symptomatic of a readjustment of demand for imports and of lower labour costs in the periphery.

By the dynamics of the international balance of payments (BoP) it is only normal to see a contraction in financial flows to fund the decreasing current account deficits of the periphery.

Labour market

As the economy has stagnated, and in some cases contracted, the new equilibrium leads to fluctuations around a higher level of unemployment. Consequently, and due to the primacy of the financial economy, unemployment has risen to levels not seen in quite some time.

In the Euro-zone, even labour variables seem to be behaving in the manner predicted by OCA theory, with migration to Germany from the periphery seeing a market increased.

Turns out things are quite predictable… Sadly so and over the right time span!

Politics: Evolving Party Systems – Responsiveness and Political Stability

In parallel to all the financial turbulence and economic contraction, political instability continued, with voters still trapped in an unresponsive golden straight jacket of national politics, fixed exchange rates and freely mobile capital.

In Ireland, Fianna Fail and Fine Gael continue to dominate, but Sinn Fein and the Independents have gained up to 10%. Labour proved very popular for some time, but this appears to have faded…

However, the best example of the complete chaos that economic and financial stability can generate is Greece, where the ongoing crisis has completely eroded the duopoly on power that PASOK and New Democracy enjoyed for the last 30 years. PASOK in particular has pretty much imploded and appears to have been replaced by Syriza as the main left-wing party. While the smaller parties that have benefitted in PASOK’s fall are mostly mild mannered, the extremist fringes of Syriza and the plain extremist Golden Dawn are particularly concerning.

However, the best example of the complete chaos that economic and financial stability can generate is Greece, where the ongoing crisis has completely eroded the duopoly on power that PASOK and New Democracy enjoyed for the last 30 years. PASOK in particular has pretty much imploded and appears to have been replaced by Syriza as the main left-wing party. While the smaller parties that have benefitted in PASOK’s fall are mostly mild mannered, the extremist fringes of Syriza and the plain extremist Golden Dawn are particularly concerning.

In Spain, the economic shock has not yet affected political affiliations in any profound manner. What we can see is a 10% rise in the support for the United Left and Union, Progress and Democracy.

In Spain, the economic shock has not yet affected political affiliations in any profound manner. What we can see is a 10% rise in the support for the United Left and Union, Progress and Democracy.

In Italy, the system is reforming itself in a similar manner to Greece, but not as violently. Italian politics has always been entertaining although not necessarily for the right reasons. It would appear that Berlusconi is out of Italian politics for some time to come, which is about time… Meanwhile, my best guess is that the centre left will ally itself with Monti and his platform’s partisans. Unless, Beppe Grillo (Italy’s Jon Stewart) and his 5 Star Movement or the Civil Revolution make more waves than expected…

In Germany, the system is as stable as the economy. Although the CDU remains the most popular party in German politics, the FDP has been all but obliterated, which ought to put a full stop to Anglo-Saxon reporter’s claims the Germans have become Eurosceptic once you consider that the FDP is the only party to have expressed such view. The CDU and the SPD as well as the Greens remain staunchly European. The next coalition government is likely to be any of the following: CDU-SPD-Greens, CDU-SPD, CDU-Greens, SPD-Greens, SPD-Greens-Pirates. Either way, Germany remains profoundly European, which should keep Austria in check.

Similarly, and despite their EU referendum shennanigans, the political system has remained relatively stable. So the support for UKIP has not really come from Labour or the Conservatism, but rather from the other parties. Meanwhile, the main shift has been from a Conservative majority to a Labour one.

Pingback: The Chinese Economy: A short guide to its Past, Present and Future | Makronom