As I mentioned earlier, in a very delayed reaction to a comment on European blogging, I’ve decided to start looking around at what other bloggers write and comment on it, while hopefully not neglecting to come up with my own content.

Because the inspiration for this new attitude came from Bruegel, I think it is only fair to begin by considering contributions published there, particularly those from Jérémie Cohen-Setton, Martin Kessler and Shahin Vallée, who authored that article. Unfortunately, only Vallee has published a relevant post lately, so I shall focus on him and 2 other authors published by Bruegel’s blog.

In this spirit I looked around for the latest contributions and found the following three articles

- From mutual insurance to fiscal federalism – rebuilding EMU after the demise of the Maastricht architecture, by Shahin Vallée

- 3) A crazy idea about Italy – Italy needs growth in nominal GDP to stop its debt burden from rising any further. To do so it needs Germany’s help, by Jim O’Neill

- 4) Are the Eurozone’s fiscal rules dying?, by Ashoka Mody

The Mutual Insurance Road to Fiscal Federalism

This article refers to the argument that the creation of the ESM and the EFSF before it is tantamount to an insufficient mutual insurance version of fiscal federalism that responds to crisis, but does not kill them on their tracks. This is the very reason of its insufficiency. Debt is mutualised only when its too expensive for the nation states to carry the burden on their own.

The author reflects on the fact that an alternative is to have genuine fiscal federalism with spending taxation and borrowing.

One benefit to having a proper federal EU debt is technical. It would generate a major European (rather than the present Franco-German state of affairs) borrower which would face much more inelastic demand. The resulting monopsony would simply allow the EU to borrow more cheaply. If you agree that there are indeed some things that the EU ought to do and that it should do it as cheaply as possible, actual debt federalisation makes a lot of sense.

Vallee also considers the path to such an arrangement. He looks, much as I did, at the path to debt mutualisation that the USA followed when it went from confederation to a federation.

Here I have to be slightly more pessimistic. Historically, fiscal centralisation (which in this case and in this case only I’m willing to equate with fiscal federalism) has not been brought about solely by debt mutualisation, although in a sense that has indeed been part of it. Instead it has been the result of defence policy, a Euphemism for war or at least military centralisation. Even in the USA’s case, I doubt the federalism arrangement would have proven so popular had it not been for the still present English threat which brough war back in 1812. Now, I have very non-bellicous reasons why this driver should motivate the EU, but not even I am optimistic enough to foresee them as being a significant driver to that end. If such a thing would come to pass, it would probably be the result of a fall from grace of USA hegemony and the rise of a Russian threat, none of which are a particularly desirable prospect.

Italian Growth Needs German Help?

In this article Jim O’Neill considers the position of Italy prior to and after joining the Euro-Zone. His comment is based around the fact that with a dysfunctional political system a very adaptive private sector was able to stay afloat and compete internationally due to devaluations. Now that Italy is in the Euro-Zone this is no longer possible and as a result, Jim argues that Italian growth has stagnated. He agrees that there are plenty of things Italy needs to do on its own, chiefly among which would be to improve its competitiveness if it wants to rein in on its rising debt. He concludes with a suggestion that “Italy could impose a punitive tax on German tourists” in order to compensate it for the fact that German inflation is overvaluing the Euro at a cost to Italy. He concludes with a suggestion that this might not be much crazier than a deflationary Europe.

So let’s consider his point, one thing at a time. First does Italy have a debt problem? The figure below, compiled through Trading Economics shows this point quite evidently. It compares Italian public debt to GDP ratios with their German counterparts (the left vertical axis if for Italy and the right is for Germany). Italy’s debt is above 130% of GDP while Germany’s is below 80%.

What’s the effect of this on the cost of debt? – The figure below shows the 10yr yields on Italian, French and German government bonds. Italy’s are the top, Germany’s at the bottom. What we see is that Italian levels are not only higher, they are also much more volatile than German (or for that sake French) ones. The difference isn’t huge (actually because of the volatility at some points in time it actually was pretty huge, veering onto Greek territory), but it is not irrelevant and certainly adds to the burden of an already burdened debtor.

So what drives bond yields? One way to think about the yield on long maturity bonds is as the present value of overnight interest rates at that point in the future. This in turn should reflect the central bank’s Policy (Taylor) Rule and thus be the result of GDP and inflation expectations. If the two are expected to grow, yields will rise, if not they will fall. What about the GDP. Is there really a huge problem as far as growth is concerned.

So what does the data show? – Well actually, considering the data it would appear to be the case as both countries seem to move in tandem. However, there is one great big difference. Whenever there is growth, Germany seems to peak above Italy, which over 10 years adds up to real money. Also since the beginning of the sovereign debt crisis, Germany has consistently outperformed Italy, which is consistent with the narrative we all know of.

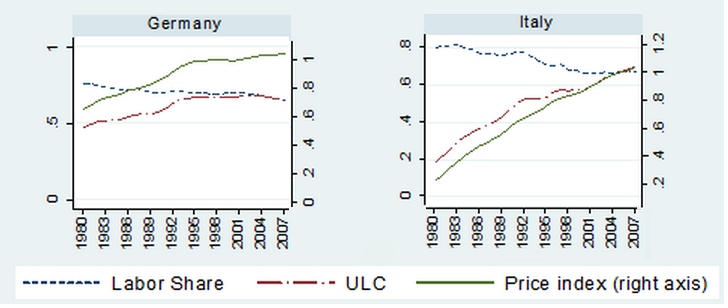

So what is driving this? Traditionally the analysis is fairly shallow and I myself have been guilty of this. The comment is always, well “Italy is riskier”, “it’s disfunctional”, “look at their PM” (not the present one, Berlusconi), “they are not competitive”. It scratches the surface but doesn’t dig down. I was recently caught doing this myself and called out on it, much to my embarrassment. It was pointed out to me that one very good metric of this problem was Unit Labour Costs. I’ve been familiar with this fact and I have even talked about it at length in relation to the fact that not all European producers compete in the same markets. This was prompted by a very interesting VoxEU article by Felipe and Kumar. However, I had never associated this with bond yields and the cost of debt. Literally, I’ve never been accustomed to thinking about yields being driven by aggregate supply side dynamics which is what this variable is used for. So what can we tell from the data?

Two things stand out. First, Italy’s unit labour costs surpassed those of Germany at some point in the late 1990s. Second the main driver of Italian unit labour costs is the labour share, which captures the productivity of the country, the number of people it takes to produce something. So Italian workers are simply less productive than their German counterparts. At the same time the price index was around the same level in 2007, but it had been growing at a much faster pace than in Germany, implying that wages were also probably rising faster (even while probably remaining below German salaries).

So Italy pays higher bond yields because it does not grow as fast as Germany, and this happens (mainly) because it is not as productive. As a result investors would expect less of a return. But wait… This makes no sense! As I said, longer maturity bond yields are supposed reflect GDP and inflation expectations through the Taylor Rule and present value of those maturities. If Italy has low expectations of growth, then I should expect it to pay lower yields. So what have I missed?

What’s missing from this simple framework is that returns (or as I’ve been calling them “yields”) occur with a certain probability. So actually we can map investor choice as under uncertainty:

where r(i) is a value of returns offered by Italy, f(r(i)) is the pdf associated with those values and U(R) is the utility derived from this consumption, so that we can model risk seeking, neutral and averse investors. So for a given level r(i) = r(g), because Italy may be less likely to pay off, due to the pdf, then in order to offer the same Utility to investors it may actually have to raise r(i) above r(g), r(i) > r(g), in order for U(R)= U(Rg). How much so this will be, will depend on the Italian and German pdfs and on the utility function of investors.

To return to our less productive Italians, it is possible to think of investors as engaging in dynamic recursive bayesian learning. If the economy is not productive, this will decrease the probability of Italy to pay its returns, so it will have to offer higher yields to offer a competitive utility vis-a-vis the safer returns offered by Germany.

So yes, I agree with Jim O’Neil’s logic, but I like it well laid out as above.

Do I think Germans should be foreced to accept higher inflation. Sure, but I don’t think they should need convincing. Why would anyone want deflation. But if that’s really what you want, get them a left-wing government keen to spend money. A conservative govenrment won’t do it. And taxing tourists is just a silly idea. I’m not sure what the elasticity of demand of tourism is, but in our age of RyanAir tourists I would expect it to be very high, so the relevant laffer curve may not be very generous in this case.

Death to the Fiscal Rules!

This article is on a the fact that the EC recently went light on France and Italy’s inability to comply with deficit targets set for EZ member states. This is a topic very dear to my heart, having myself spent some time researching the SGP, fiscal multipliers and fiscal federalism. Fiscal rules have about as much credibility as fixed exchange rates, with an added political aspect that large important countries, such as France and Italy, tend to have an easier time getting away with it than say Portugal and Greece. This was the case in 2003-4 when Portugal and Greece became some of the first countries to be threatened with fines by the EC for not complying with the rules only to see those threats withdrawn when France and Germany were shown to also be at fault. Finally, centralisation of rules tends to trigger collective action problems and asymmetries of information that are ripe for corruption, fiscal mismanagement and undermining of representative democracy.

So when the author cites Delors who said that “centralization of fiscal rules makes neither economic nor political sense” and that “Persisting with centralized fiscal rules despite their evident costs—because all other options have been ruled out—is a grievous error”, I could not agree more.

Where I disagree is in the limited scope of his conclusions which argue that the solution is an ECB as a lender of last resort and better debt restructuring (or what we may want to call debt restructuring) procedures. I agree with these, but I would add a (very) limited layer of fiscal federalism, so that transfers from the rich (citizens, not countries) to the poor could take place and manage asymmetric shocks. This would have the added effect of easing the fiscal burden of nation-states and reinforce the fiscal capacity of the EU, allowing for the exploitation of economies of scale, while still allowing for a layered fiscal system where national governments could still compete. This is basically be what Vallee calls Musgrave’s (1959) stabilisation function, or what we now call automatic stabilisers as I mentioned before.